Table of Content

Insurers use a variety of factors to price homeowners insurance rates. For example, you might pay more if you live in a neighborhood with a high crime rate or in an area prone to hurricanes. You’ll also have higher rates if you have a larger home that needs more coverage. Here’s how filing a claim could affect your homeowners insurance costs. Our sample policy includes $300,000 of dwelling coverage, $300,000 of liability coverage and a $1,000 deductible. The cost of your own homeowners insurance will depend on your location, the size of your house and how much coverage you need.

That’s the average for a home insurance policy with $300,000 in dwelling coverage, $300,000 in liability insurance and a $1,000 deductible. Flooding is a natural disaster that can strike any part of the country at any time. In this blog post, we will explore how to calculate flood insurance premiums and help you understand what you’re paying for. From damaged property to lost income, read on to learn everything you need to know about flood insurance. Anyone in the process of purchasing a home is intimately familiar with the effect their credit score has on interest rates and borrower’s fees. Credit score may also impact a homeowners insurance policy premium.

Why did my home insurance go up?

The cost of homeowners insurance can be remarkably flexible based on what is being insured, and there are several ways to lower homeowners insurance rates by making a few smart decisions. First, if a homeowner has a mortgage, lenders will most likely require them to carry homeowners insurance. From the borrower’s end, that’s one less bill to pay, but it also means that it’s easy to forget to review coverage periodically, which is important.

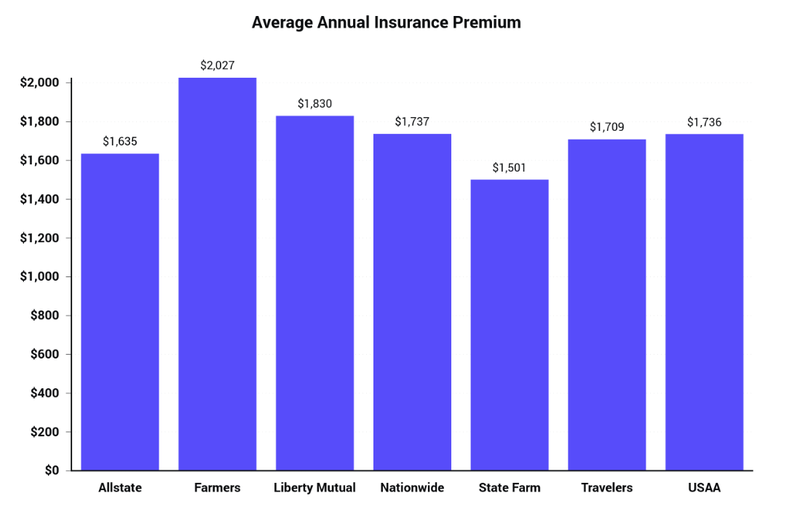

Credit scores can be an indicator of risk, as studies show that those with lower credit scores tend to file more claims compared to those with higher credit scores. For this reason, home insurance for people with bad credit is generally more expensive compared to those with average, good and excellent credit scores. Below you will find premium data provided by Quadrant Information Services for different coverage selections. We’ve also included our Bankrate Score to help you understand how these companies ranked based on several metrics, including average rate, J.D.

How much is homeowners insurance in California?

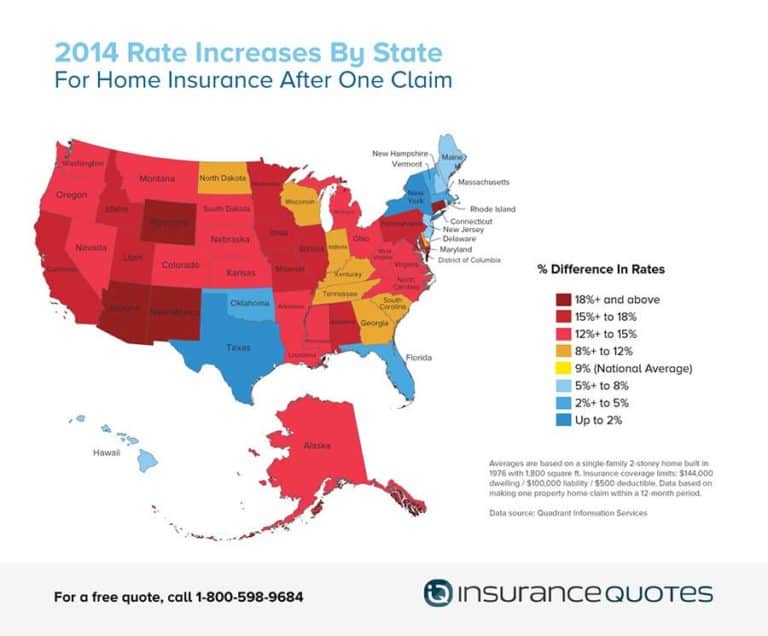

The state representatives tell us that while Florida accounts for only 16% of the insurance market claims, we are responsible for 76% of the litigation. I wonder how much of that is due to the awful way insurance companies operate here. I hope the well-off enjoy mowing their own lawns and fixing their own cars and homes because those of us who do the actual work will no longer be able to afford living here. Our analysis found that the average home insurance cost is less than $1,000 in some states, including Hawaii, Delaware and Vermont.

Real estate, famously, is all about location, location, location. The least expensive ZIP code for homeowners insurance is in Honolulu, Hawaii, at $579 a year on average. Whereas – Rosenberg, Texas – is the most expensive ZIP code for home insurance. Its average annual rate is $6,638 per year, over $6,000 more expensive than the least expensive ZIP code. To calculate your flood insurance premium, first determine your homeowners insurance policy’s base flood rate.

How much is homeowners insurance on a $200,000 house?

They simply increase the risk of claims, so you pay more for insurance. The amount you pay for homeowners insurance is determined by many factors. And the cost varies depending on the individual, but it typically requires enough dwelling coverage to rebuild one's home and enough personal property protection for their belongings. The average yearly cost of homeowners insurance is $2,777 for a dwelling coverage of $300,000 and liability coverage of $300,000 based on 2022 rates. As you’ll see in the homeowners insurance cost by state chart below, Oklahoma is the most expensive state for home insurance with a rate$2,540higher than the national average for the coverage level analyzed. We show average home rates for three other common coverage levels further down the page.

Generally, the higher your deductible, the less you’ll pay in home insurance premium. That’s because your insurance company will pay out less money if you file a claim. A standard home insurance policy (called an HO-3) covers your house for any type of damage that’s not specifically excluded.

While the national average cost of homeowners insurance is $1,383 per year, that can vary widely by region and due to other components. It’s important for homeowners to consider the house’s style and location, and then the various optional factors, before seeking out a homeowners insurance quote. A homeowners insurance calculator can help homeowners account for each of these potential costs.

Founded in 1976, Bankrate has a long track record of helping people make smart financial choices. We’ve maintained this reputation for over four decades by demystifying the financial decision-making process and giving people confidence in which actions to take next. Bankrate has partnerships with issuers including, but not limited to, American Express, Bank of America, Capital One, Chase, Citi and Discover. These are sample rates generated through Quadrant Information Services. Many or all of the products featured here are from our partners who compensate us.

At a dwelling coverage of $200,000, the average rate is $2,233, while a policy with $500,000 in dwelling coverage averages $3,594. “The other major ways to achieve a better price include investing in the condition of the property itself, such as renovating its roof or other household systems. Naturally, while this will save you money on your home insurance, the cost of the renovations themselves can’t be ignored,” Faschi adds. The most comprehensive coverage option, HO-5 covers everything that is not explicitly excluded in the policy.

If you find discrepancies with your credit score or information from your credit report, please contact TransUnion® directly. The average rate for a house with $200,000 in dwelling coverage is about $2,233 for $300,000 in liability. “One major factor in Hawaii is the fact that most standard homeowner insurance policies do not cover hurricane damage.

Just be sure to talk to a licensed insurance agent before making any changes to your home insurance. Home insurance is a many-faceted product and while $250,000 in dwelling coverage may be sufficient for some homeowners, it may not be enough for others. Your home’s characteristics, your location and local labor costs are among some of the factors that may determine how much you pay for coverage . The average annual home insurance premium for a home with a dwelling coverage amount of $250,000.

No comments:

Post a Comment